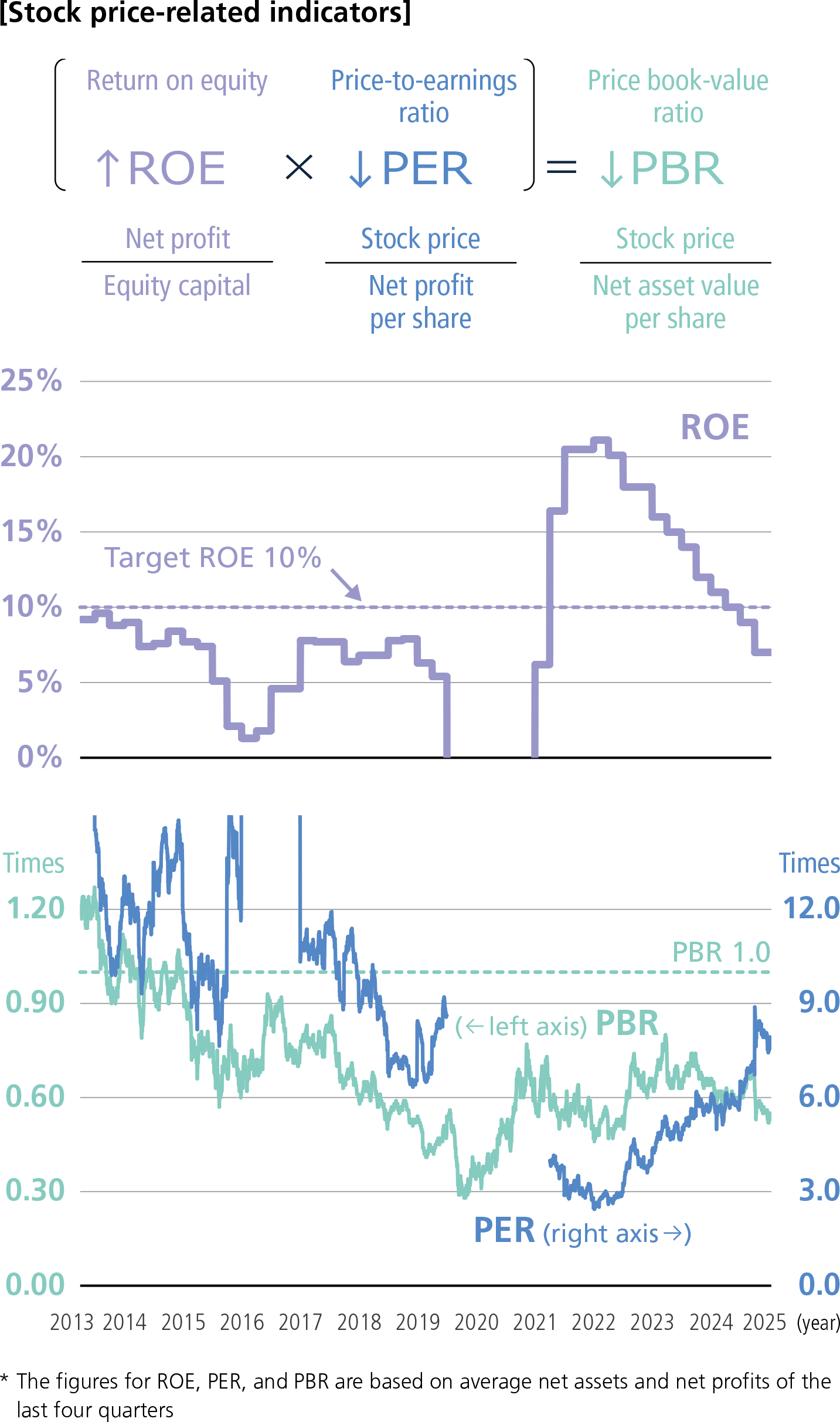

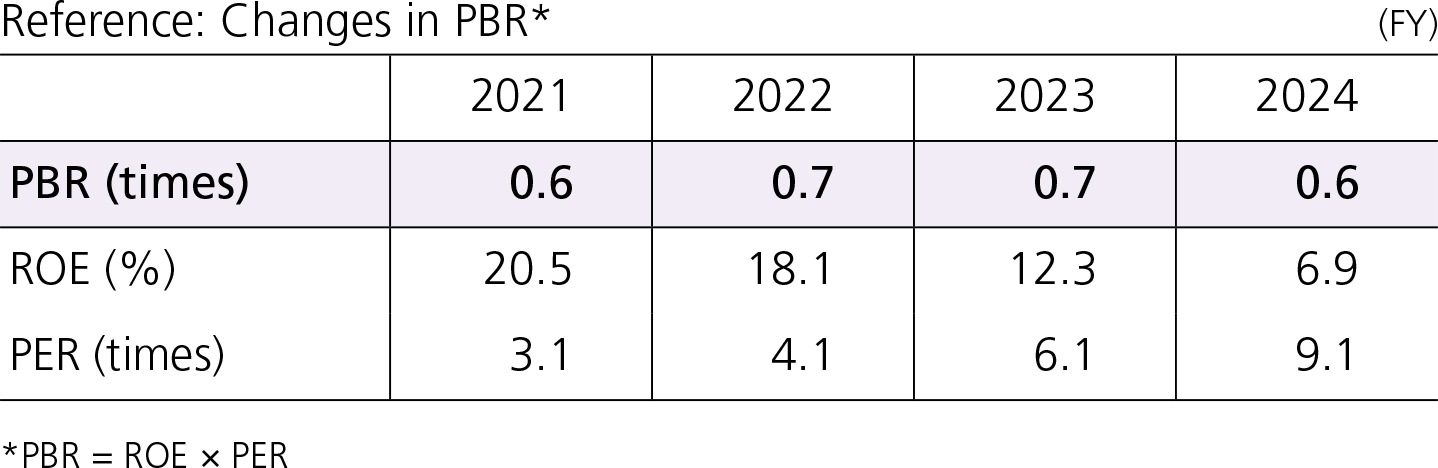

Action to Implement Management that is Conscious of Cost of Capital and Stock Price

Basic approach to improving the PBR share price indicator

The Tokyo Stock Exchange requires companies whose price-book value ratio (PBR) consistently falls below 1.0 to disclose their capital efficiency improvement initiatives and the progress thereof.

Nippon Steel is taking strategic measures to address this by focusing on ROE (capital efficiency) and PER (market valuation), the two factors that constitute PBR. We aim to consistently maintain a PBR in excess of 1.0 not only by achieving numerical targets but also by enhancing intrinsic corporate value through sustainable profit generation and building trust with the market.

Recognition of issues and approaches to be taken (Approaches from both ROE and PER perspectives)

Current status of ROE and approaches to be taken

Nippon Steel’s ROE is on a downward trend for the following reasons.

(1) Factors beyond our control, such as inventory valuation differentials, specific disclosure items, and the utilization of carry-forward losses, had a positive impact in FY2021 and FY2022 but a negative impact in FY2023 and FY2024.

For this reason, ROE appears high for FY2021 and FY2022, and conversely, ROE appears low for FY2023 and FY2024. For reference, the ROE for FY2024 exceeds 9% if inventory valuation differentials and specific disclosure items are corrected.

(2) While appropriately returning our earnings to our shareholders, we are in the process of actively investing them in future growth by capturing business opportunities.

As our basic policy, we make investment decisions to ensure their returns exceed the cost of capital. However, it takes a certain amount of time for investments to generate returns. Because of this, our capital efficiency indicators temporarily deteriorate as we make continuous investments for growth, but these investments are essential for our long-term growth. We believe this approach represents sound management judgment.

In addition, given the expected significant increase in liabilities from the merger with U. S. Steel, we have intentionally not considered capital measures in light of our future financial foundation. Furthermore, the scale of our profits has decreased due to the recent unprecedented deterioration of the business environment. These are also the reasons why our ROE is low.

It will take some time before we reach the point of recovering these investments due to planned short-term significant investments for future growth. However, following the implementation of effective permanent financing related to the U. S. Steel merger, we will steadily make investments that will lead to future growth, including capital investments in U. S. Steel. This will enable Nippon Steel to generate the intended returns from growth investments and strive for medium- to long-term improvements in capital efficiency.

Current status of PER and approaches to be taken

Conversely, Nippon Steel’s PER is trending upward. We believe this is because our initiatives to date are gaining traction in the market. In addition to continuing these efforts in the future, we believe it is also necessary to implement measures that address the concerns of our shareholders and investors regarding our initiatives to achieve carbon neutrality.

We will improve our PER further by enhancing our integrated reports, which also contain information on ESG, and financial IR materials. We will also expand IR activities for individual investors, and continue strengthening communications with domestic and overseas institutional investors. To ensure the feasibility and economic viability of the Carbon Neutral Vision, we will continue to devote efforts to enhancing shareholders’ and investors’ understanding of the current status and outlook of our carbon neutrality initiatives through technological development, commercial-scale implementation, and the establishment of a GX Steel market.